Cash Book Description

A cash book is a financial ledger used by businesses and individuals to record their cash transactions. It serves as a record of all inflows and outflows of cash, providing a detailed overview of the organization's or individual's cash position.

In its simplest form, a cash book consists of two columns: one for cash receipts (inflows) and another for cash payments (outflows). Each transaction is recorded with a date, description, amount, and the relevant column (receipt or payment). The cash book is typically updated regularly, either daily, weekly, or monthly, depending on the volume of transactions.

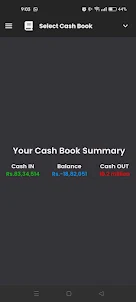

The purpose of maintaining a cash book is to track the movement of cash and monitor cash balances accurately. It helps in managing and controlling cash flow, identifying any discrepancies or errors, and providing a record for reference and reconciliation purposes. Additionally, a cash book serves as a primary source of information for preparing financial statements like the income statement and balance sheet.

In its simplest form, a cash book consists of two columns: one for cash receipts (inflows) and another for cash payments (outflows). Each transaction is recorded with a date, description, amount, and the relevant column (receipt or payment). The cash book is typically updated regularly, either daily, weekly, or monthly, depending on the volume of transactions.

The purpose of maintaining a cash book is to track the movement of cash and monitor cash balances accurately. It helps in managing and controlling cash flow, identifying any discrepancies or errors, and providing a record for reference and reconciliation purposes. Additionally, a cash book serves as a primary source of information for preparing financial statements like the income statement and balance sheet.

Open up